Key Innovation

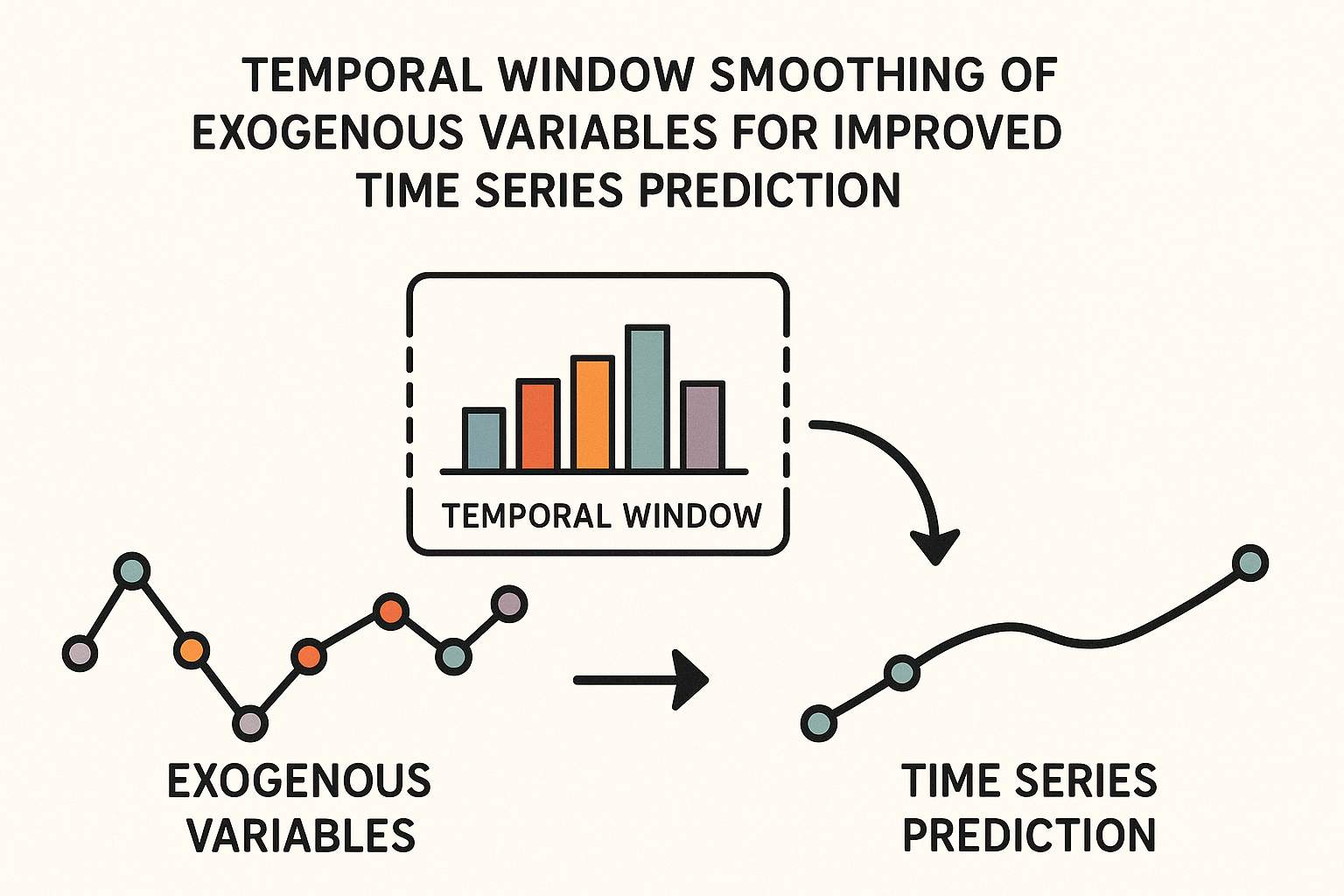

Our research team at RobotBulls has developed a novel preprocessing technique that significantly improves time series prediction accuracy by applying temporal window smoothing to exogenous variables, reducing noise and capturing more stable underlying patterns.

The Challenge

Time series prediction is fundamental to many real-world applications, from financial forecasting to climate modeling. However, the accuracy of these predictions often suffers when external factors (exogenous variables) introduce noise and instability into the models. Traditional approaches struggle to effectively filter out short-term fluctuations while preserving meaningful signals.

Our Solution: Temporal Window Smoothing

Our research, conducted by Mustafa Kamal, Niyaz Bin Hashem, Robin Krambroeckers, Nabeel Mohammed, and Shafin Rahman, introduces a sophisticated yet elegant solution: Temporal Window Smoothing (TWS). This technique processes exogenous variables through a carefully designed temporal window, effectively:

- Reducing noise from short-term market fluctuations

- Preserving important trend information

- Extracting stable, meaningful patterns from volatile data

- Improving the signal-to-noise ratio of input features

What Are Exogenous Variables?

In time series analysis, exogenous variables are external factors that influence your primary prediction target. For example, when predicting stock prices (endogenous), factors like market indices, economic indicators, or social sentiment (exogenous) can provide valuable context. Our method ensures these external signals enhance rather than confuse the prediction model.

Technical Innovation

The core innovation lies in our adaptive smoothing algorithm that:

- Dynamically adjusts the smoothing window based on data characteristics

- Preserves critical events while filtering routine noise

- Maintains temporal relationships between multiple exogenous variables

- Scales efficiently for high-dimensional time series data

Real-World Applications

This breakthrough has immediate applications across multiple domains:

- Financial Markets: More accurate prediction of asset prices and market trends

- Supply Chain: Better demand forecasting and inventory optimization

- Energy Sector: Improved load forecasting and grid management

- Healthcare: Enhanced patient outcome predictions using multiple vital signs

- Climate Science: More reliable weather and climate projections

Results and Impact

Our experiments demonstrate substantial improvements in prediction accuracy across diverse datasets. The temporal window smoothing approach consistently outperforms traditional preprocessing methods, with particularly strong results in volatile, noise-prone environments where conventional techniques struggle.

By focusing on the preprocessing stage rather than model architecture, our method can be integrated with any existing time series prediction framework, making it widely accessible and immediately applicable to current systems.

Integration with RobotBulls Trading Systems

This research directly enhances RobotBulls' AI-powered trading algorithms. By applying temporal window smoothing to market indicators, economic data, and sentiment signals, our trading bots can make more informed decisions, filtering out market noise while capturing genuine trend shifts. This leads to more stable returns and reduced false signals in volatile market conditions.

Future Directions

Our team is actively exploring extensions of this work, including:

- Adaptive window sizing based on market volatility

- Multi-scale temporal smoothing for different time horizons

- Integration with deep learning architectures

- Real-time implementation for high-frequency trading applications

Access the Full Research

For technical details, mathematical formulations, and comprehensive experimental results, we invite you to read our complete research paper. This work represents a significant step forward in time series prediction methodology and opens new possibilities for accurate forecasting across multiple domains.

Read the Full Research Paper on arXiv →

This research was conducted by the RobotBulls AI Research Team in collaboration with academic partners. For inquiries about implementing this technology in your systems, please contact our research division.